Today, the Federal Reserve maintained its 0.00%-0.25% target for the federal funds rate. However, on balance, the Federal Reserve's Federal Open Market Committee (FOMC) was somewhat more upbeat than in June.

Several highlights from the FOMC’s

monetary policy statement included:

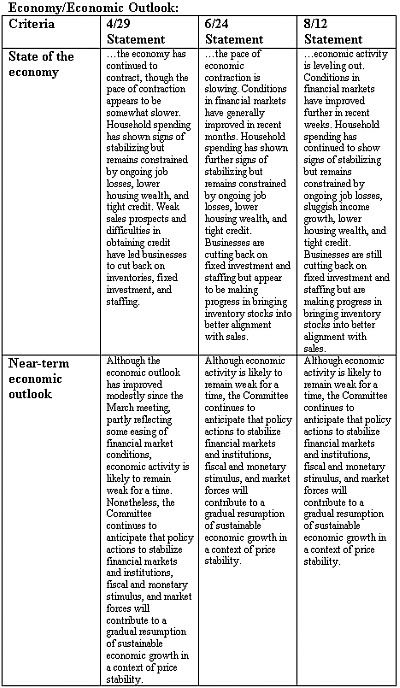

• The FOMC noted that economic activity is "leveling out." In its June 29 statement, the FOMC observed that "the pace of economic contraction is slowing."

• The FOMC reaffirmed its earlier assessment for a "gradual resumption of sustainable economic growth."

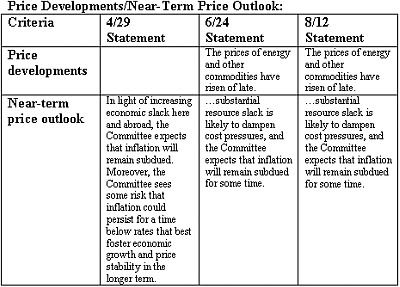

• On the inflation front, the FOMC explained that despite a recent uptick in energy and commodities prices, inflation should remain "subdued for some time."

• In maintaining its current interest rate posture, the FOMC reaffirmed its earlier forecast that "economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period."

• In a prudent move to avoid the risks associated with a premature unwinding of its extraordinary policy measures, the Federal Reserve reaffirmed its asset acquisition parameters. The FOMC also added specificity to its earlier statements, replacing "up to $300 billion of Treasury securities" with "$300 billion of Treasury securities" and "by autumn" with "by the end of October." Previously, the program was set to expire at the end of September and some market pundits had speculated that the Fed would announce an end to its asset purchases.

All said, the Fed acknowledged increasing indications of economic stabilization, but also erred on the side of caution in explaining that it will purchase the full amount of the $300 billion in Treasury securities that it had previously suggested that it could purchase.

Reflecting the strong consensus in the decision, there were no dissents.

Overall, the somewhat more upbeat economic assessment and continuity in monetary policy was consistent with my overall expectations. On August 10, my blog entry outlined my

expectations for the FOMC’s August 12 monetary policy statement. A comparison between those expectations and the wording in the FOMC’s statement follows:

Expectation: That the pace of economic contraction has slowed significantly and that economic activity is showing some indications of stabilizing. It may also note some enhancement in economic prospects. That wording will constitute an improvement over the FOMC’s June 24 statement in which it observed that “the pace of economic contraction is slowing.”

Outcome: The FOMC explained, “Information received since the Federal Open Market Committee met in June suggests that economic activity is leveling out.”

Expectation: That the housing market has shown additional signs of stabilizing.

Outcome: The FOMC’s statement made no mention of housing market conditions.

Expectation: Household spending has remained fairly stable, but is constrained by continuing weakness in the labor market.

Outcome: The FOMC explained, “Household spending has continued to show signs of stabilizing but remains constrained by ongoing job losses, sluggish income growth, lower housing wealth, and tight credit.

Expectation: Anticipation that “policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability.”

Outcome: The FOMC predicted that “policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability.”

Expectation: Modest growth in economic activity is likely during the remainder of the year.

Outcome: The FOMC provided no additional commentary on economic growth except that it expected “a gradual resumption of sustainable economic growth.”

Expectation: That inflation will remain “subdued.”

Outcome: The FOMC indicated that “inflation will remain subdued for some time.”

Expectation: The FOMC “will employ all available tools to promote economic recovery and to preserve price stability,” “will continue to evaluate the timing and overall amounts of its purchases of securities in light of the evolving economic outlook and conditions in financial markets,” and that it will monitor “the size and composition of its balance sheet” and make such adjustments as might be warranted.

Outcome: The FOMC reaffirmed all of the above ideas.

Expectation: Economic conditions will “likely warrant exceptionally low levels of the federal funds rate for an extended period.”

Outcome: The FOMC indicated that “economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”

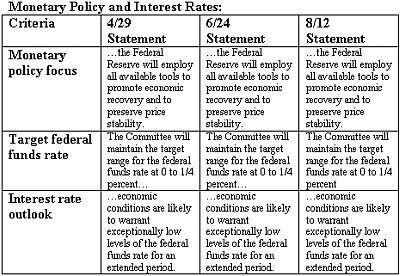

Finally for purposes of comparison, the following tables reflect the Fed’s evolving thinking on key criteria from the April 29, June 24, and August 12 monetary policy statements.

Extraordinary Programs/Fed’s Balance Sheet:

Extraordinary Programs/Fed’s Balance Sheet:

&&